Fourth Quarter 2018 Results: Bio-Rad Laboratories, Bruker, Danaher and Thermo Fisher Scientific

Bio-Rad Life Science Revenue Soft Due to RainDance and Process Media Products Sales Decline

Q4

Click to enlarge

Sales for Bio-Rad Laboratories’ Life Science segment increased 0.7% on an organic basis. The business segment’s revenue growth was driven by demand for cell biology, Western blot and digital PCR products, as well as gene expression and antibody products. The growth was offset by the expected decline of the process media product line and the reduction of sales of RainDance products. The combined decline sales of RainDance and process media products was $8 million, with each declining $4 million. Excluding currency, Life Science experienced strong revenue growth in the US and China.

FYE

Click to enlarge

Sales for Bio-Rad Laboratories’ Life Science segment increased high single digits on an organic basis. The business segment’s revenue increase was driven by double-digit revenue growth of Droplet Digital PCR products, cell biology and food safety products. Other highlights included returned demand for Western blot and process media products, notwithstanding the $4 million decline for the fourth quarter 2018.

Geographically, Life Science saw broad-based demand, fueled by double-digit revenue growth in the US and China. For full-year 2019, Bio-Rad anticipates its Life Science revenue to increase 5.0%–6.0%. This outlook is anticipated from the broad-based growth for its product lines and the regions it serves, despite expectations of a $9 million sales decline of RainDance products.

Bruker’s BSI Revenue Slowdown Due to Low Sales in Europe and China

Q4 and FYE

Fourth quarter 2018 Bruker Scientific Instrument (BSI) sales increased to make up 91% of company revenues (see IBO 02/15/19). System sales grew 1.7% to account for 73% of total revenues, while Aftermarket sales jumped 8.1%.

Click to enlarge

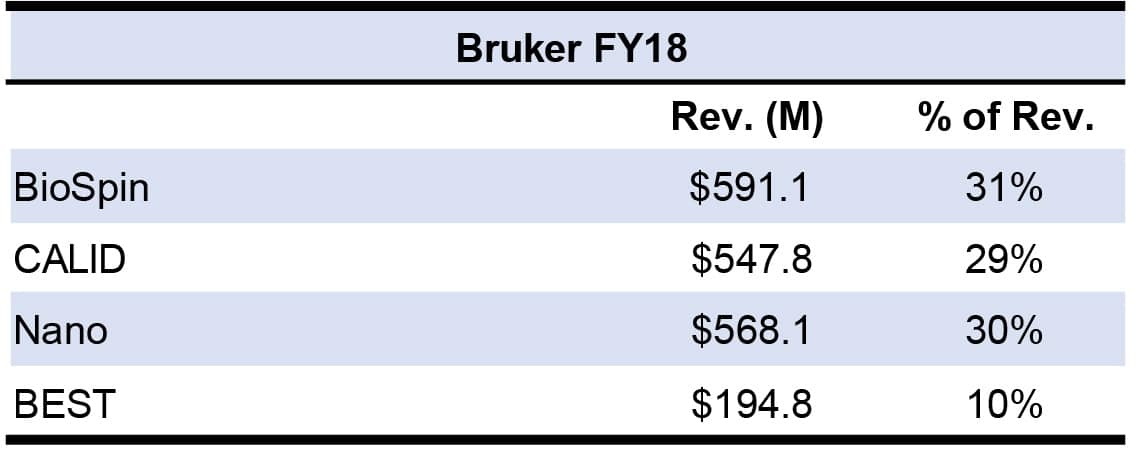

Full-year 2018 BSI sales increased to make up 84% of company revenues. System sales grew 6.7% to account for 72% of total revenues, while Aftermarket sales jumped 10.6%. Organic revenue growth was led by strong sales for the Nano and CALID groups.

Click to enlarge

End-market wise, Bruker saw broad-based demand across all markets throughout the entire year. However, there was a significant sales decline of the semiconductor metrology business during the fourth quarter 2018 and latter half of 2018. Semiconductor metrology sales made up 5% of the company’s total revenues.

Click to enlarge

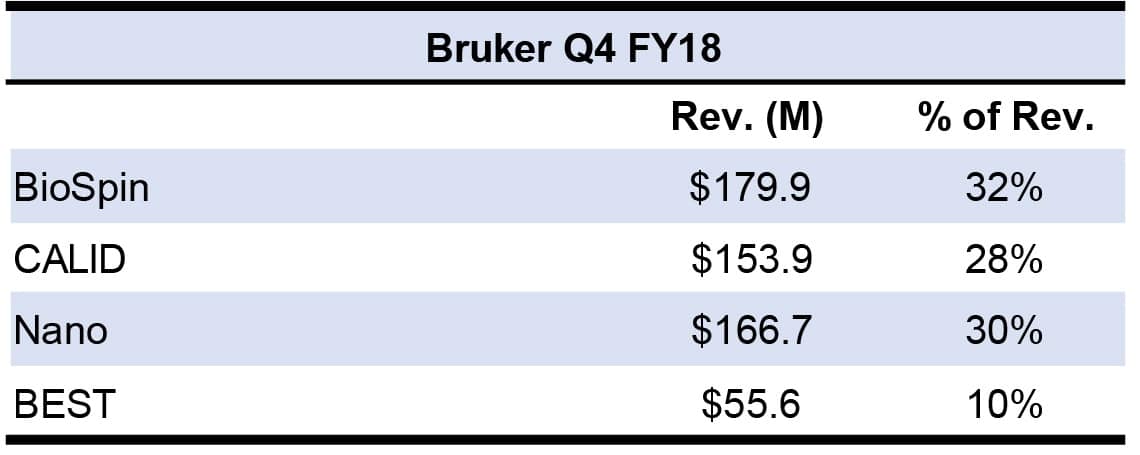

For fourth quarter 2018, the BSI segment delivered low-single-digit revenue growth due to the company focusing on de-risking for full-year 2018 financial results. For 2018, the BSI segment delivered mid-to-high single digit organic growth including solid sales in the last quarter. Sales were led by demand for the CALID and Nano Groups, as well as from North America and China.

Click to enlarge

BioSpin experienced a revenue increase in the low single digits due to the broad-based sales to the biopharma, clinical and applied markets and aftermarket sales. Strong sales in these markets offset the soft sales in the academic and government markets. In addition, BioSpin’s NMR system sold modestly, while sales for applied and clinical phenomics were consistent. Also, the division’s NMR and preclinical imaging aftermarket and service revenues rose in the high single digits.

Click to enlarge

CALID sales increased high single digits, driven by solid demand for MS, molecular spectroscopy, microbiology and diagnostic product lines. Regarding MS, Daltonics product sales increased significantly thanks to strong demand for its microbiology and life science MS portfolios. Life science MS portfolio sales were led by the solid performance of the QTOF MS portfolio. The microbiology and diagnostics portfolio were led by broad-based sales of its instruments, consumables and services, while molecular spectroscopy business sales were driven by solid demand within its end-markets. Due to the continuing sluggish sales of CALID’s detection product line, Bruker began a restructuring program that will consolidate it within CALID’s optic business. CALID’s detection product line delivered approximately $30 million in revenue in 2018.

Click to enlarge

Nano sales were fueled by solid sales of the division’s ADVANCE x-ray products in industrial, materials research and academic and government markets. Other highlights include the increased sales of Nano Surfaces and Nano-analysis tools. These product lines’ strong sales offset the sales declines of the Nano-semiconductor metrology product line due to the overall slow demand for the company’s semiconductor metrology product line.

Click to enlarge

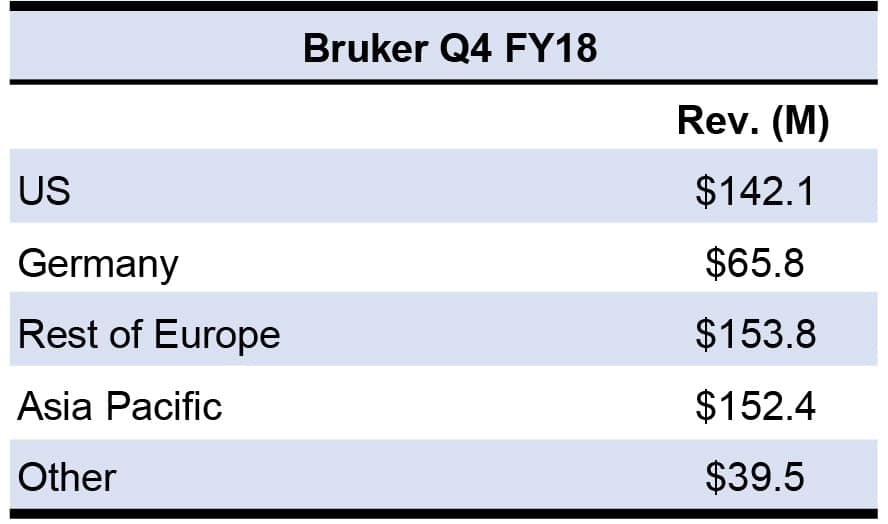

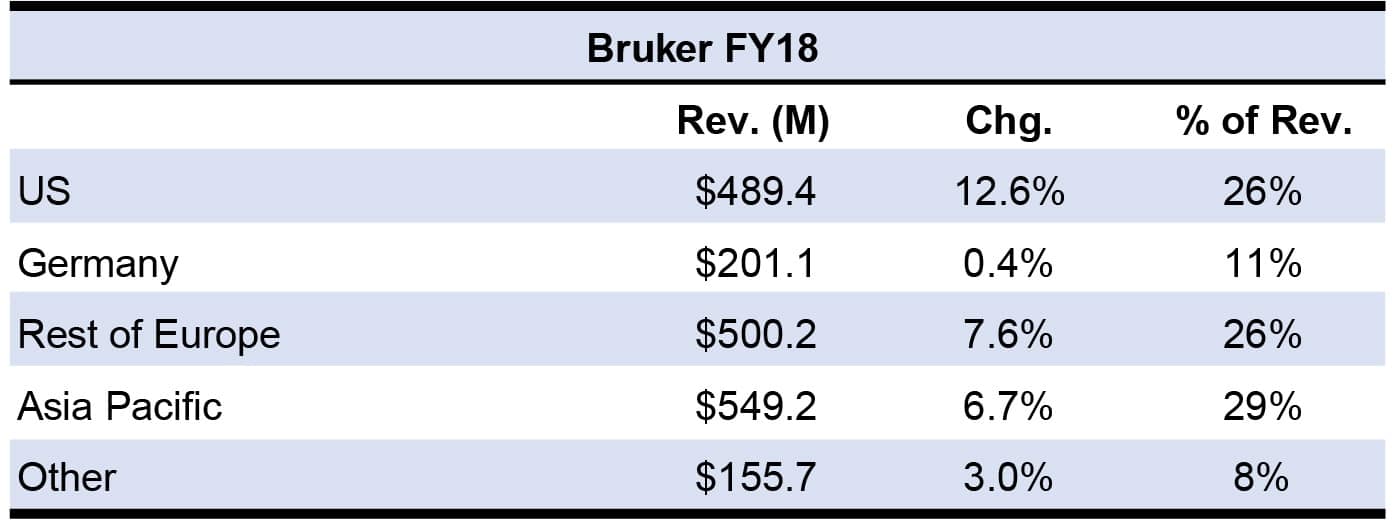

By region, European BSI sales rose modestly with low-single-digit growth, while North American BSI sales rose low double digits. Asia Pacific sales rose in the mid-single digits, with flat Chinese sales only delivering low-single-digit growth. However, BSI orders in China remained robust throughout fourth quarter and full-year 2018.

Click to enlarge

For full-year 2019, Bruker forecasts its revenue to grow 6%–7%, including 4%–5% organic revenue growth and 8%–9% grown on a constant currency basis. This includes a 4% acquisition contribution. Geographically, the company expects double-digit growth in China as well as a solid performance in the US, while having lower expectations for Europe due to the region’s long pattern of annual low-single digits revenue growth. End-market wise, Bruker anticipates biopharma’s sales to be led by NMR and MS sales while expecting the applied market to have strong product sales for NMR, optics, microbiology, infectious disease diagnostics and the aftermarket business. However, Bruker does anticipate a slight decline in sales for the applied end-market as well as industrial. Product-wise, the company expects revenue tailwinds from proteomics and timsTOF Pro sales, and is also expecting sales for fluorescence microscopy portfolio for neuroscience and cell biology.

Bruker did not provide first quarter company or BSI revenue guidance, but the company stated that it anticipated a 5% currency headwind for the first quarter.

Danaher’s Beckman Life Science Sales Led by Automation

Q4 & FYE

Click to enlarge

Click to enlarge

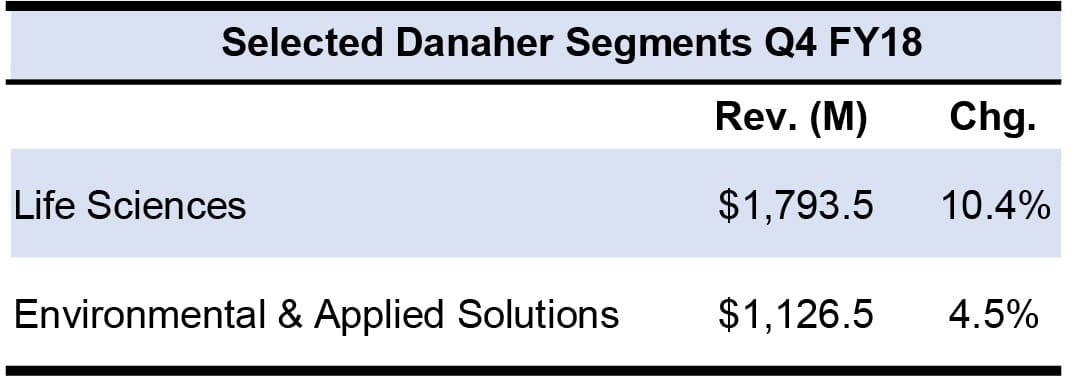

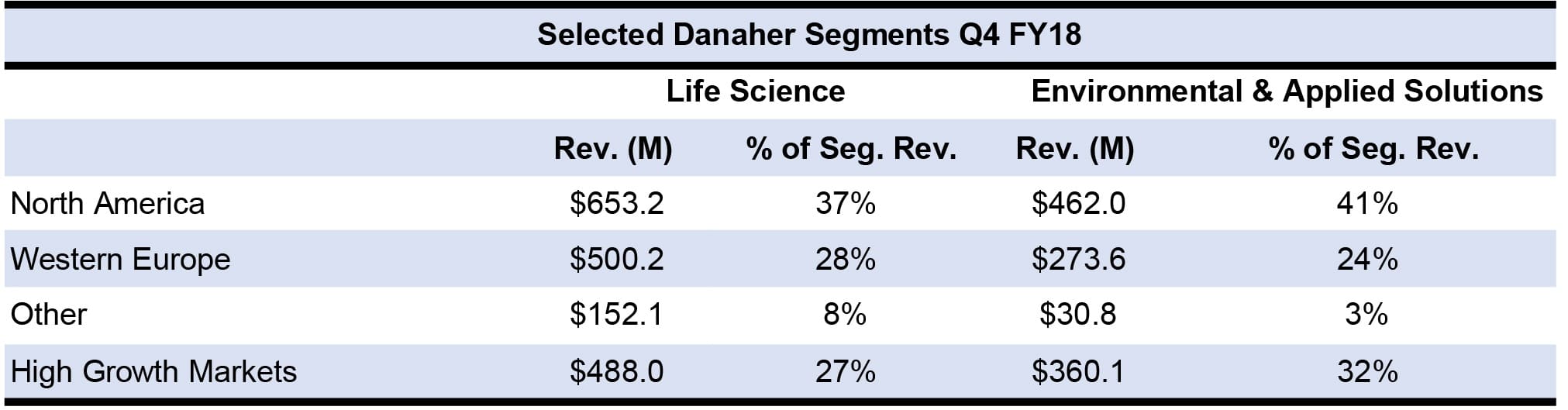

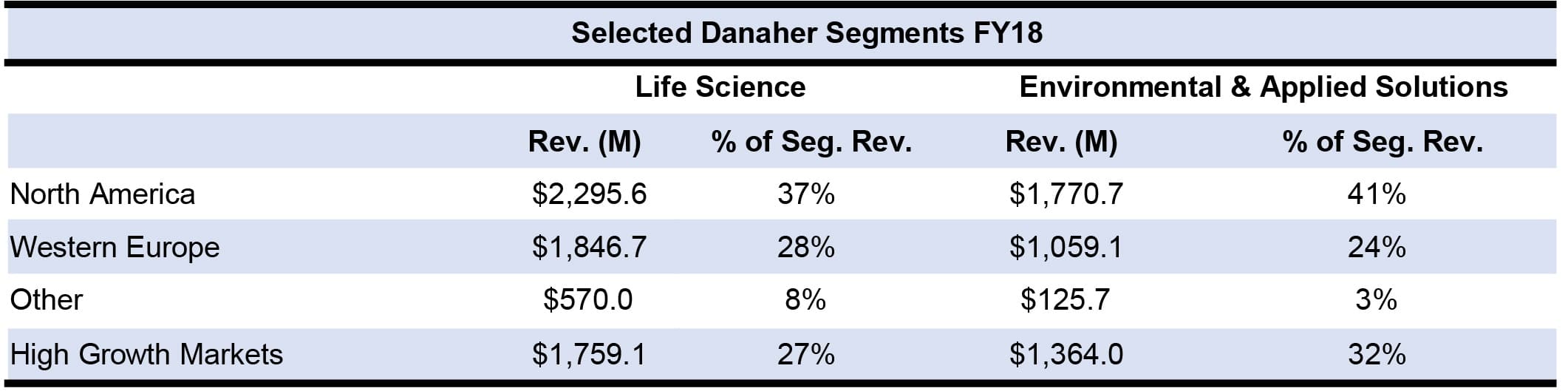

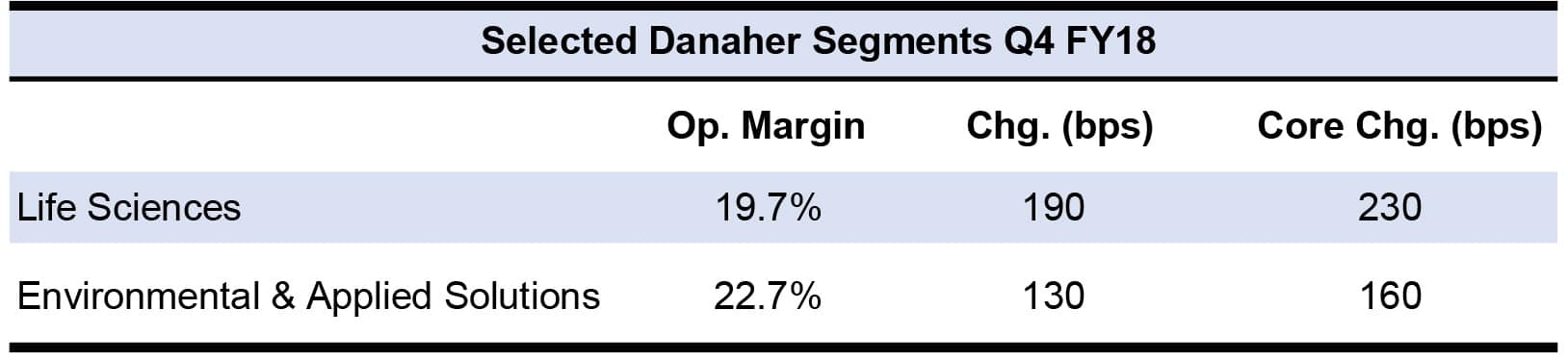

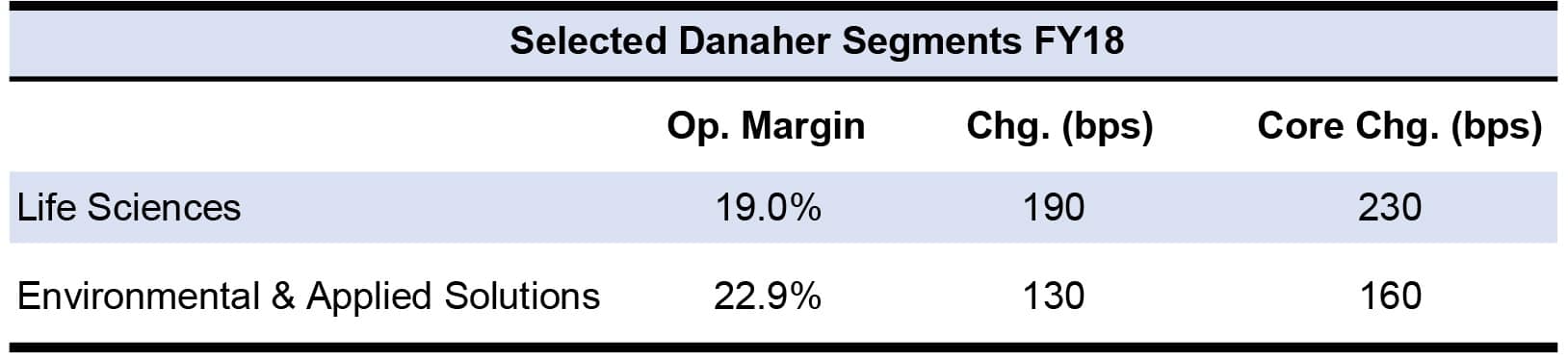

Danaher’s 5.5% revenue growth with core growth of 5.5% for the fourth quarter 2018, was led in part by 10.5% revenue growth with core growth of 7.5% for the Life Sciences business (see IBO 01/31/19). Life Sciences’ operating profit margin declined 19.7% due to foreign exchange headwinds and investments including in R&D spending and sales and marketing. Danaher’s 8.5% revenue growth with core growth of 6.0% for the full-year 2018 was led in part by 13.3% revenue growth for the Life Sciences business.

Click to enlarge

Click to enlarge

Within the Life Sciences segment, Beckman Life Sciences’ revenue rose high single digits due to 20% revenue growth in automation. Specifically, automation revenue growth was led by demand for new products such as the Biomek i-Series, a liquid handling system. SCIEX revenue grew high single digits, with solid sales in North America and China. Marketwise, demand was high in the clinical, food testing and forensics markets.

Also, within the Life Sciences segment, Leica Microsystems’ revenue was up mid-single digits due to broad-based growth across all markets and regions, led by life science research in North America. Phenomenex’s revenue rose high single digits, while biotech sales were up double digits. Pall’s revenue rose high single digits, driven by demand across the life sciences and industrial markets, with demand led by single-use technologies. IDT experienced broad-based growth across all major regions and product lines which resulted in a mid-teens revenue increase.

Click to enlarge

Click to enlarge

Within the Environmental and Applied Solutions segment, water quality sales were up mid-single digits, including high single-digit revenue growth for Hach. The business’ revenue growth was attributed to demand in the municipal and industrial markets, led regionally by China. For the full-year 2018, Hach’s revenue grew 10%. Danaher forecasts both its first quarter revenue and full-year 2019 revenue to increase approximately 4%.

Thermo Fisher Scientific’s Life Science Solutions Sales Led By Bioproduction, BioScience and Clinical NGS

Q4

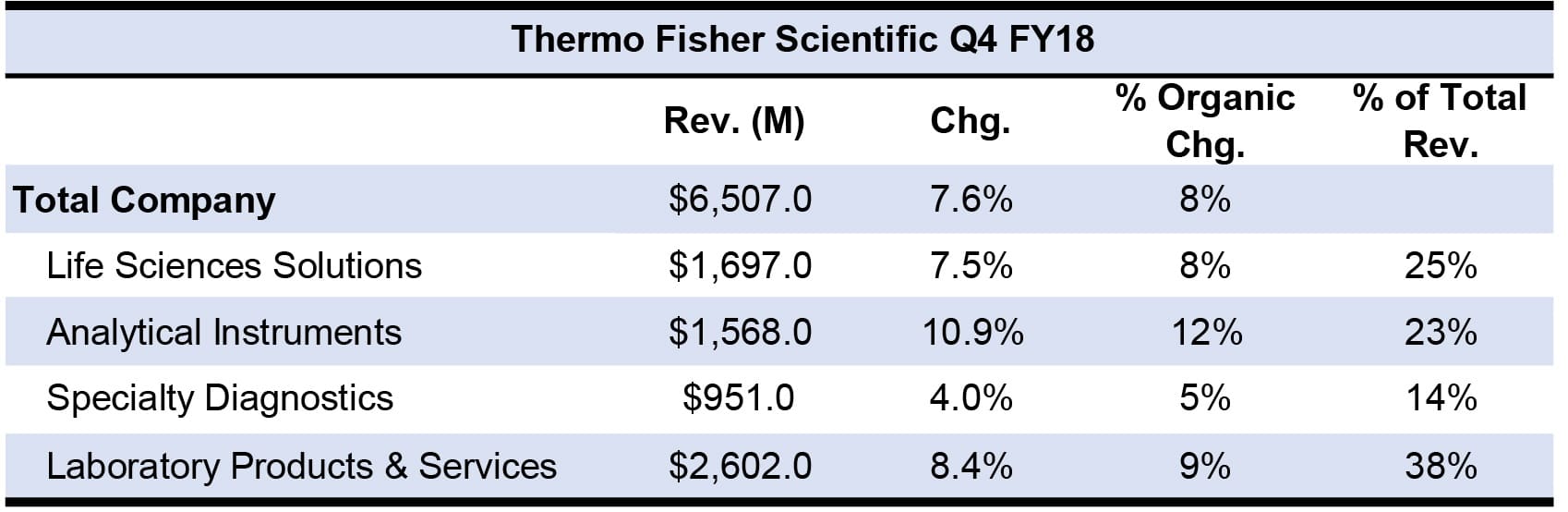

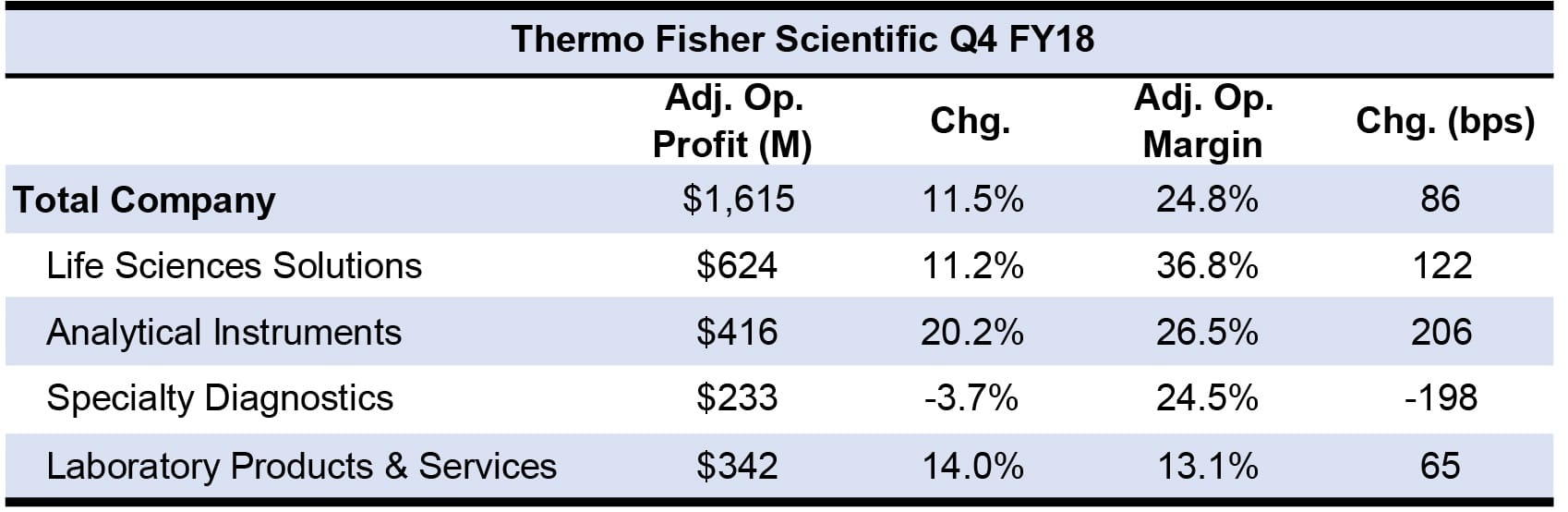

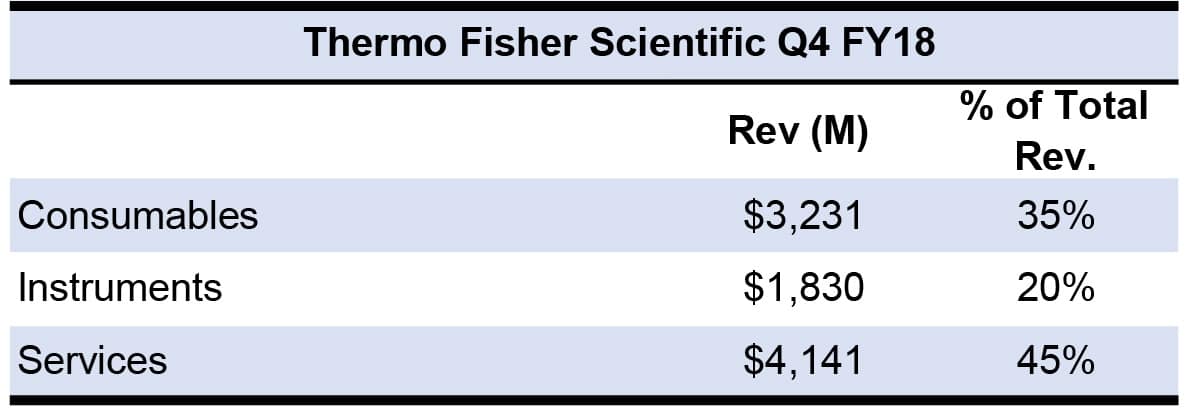

Reported high single-digit fourth quarter 2018 revenue growth for Thermo Fisher Scientific included 1% growth from acquisitions and a 2% decrease from currency (see IBO 01/31/19). The company credited the revenue growth to strong market conditions and improved operational execution.

Click to enlarge

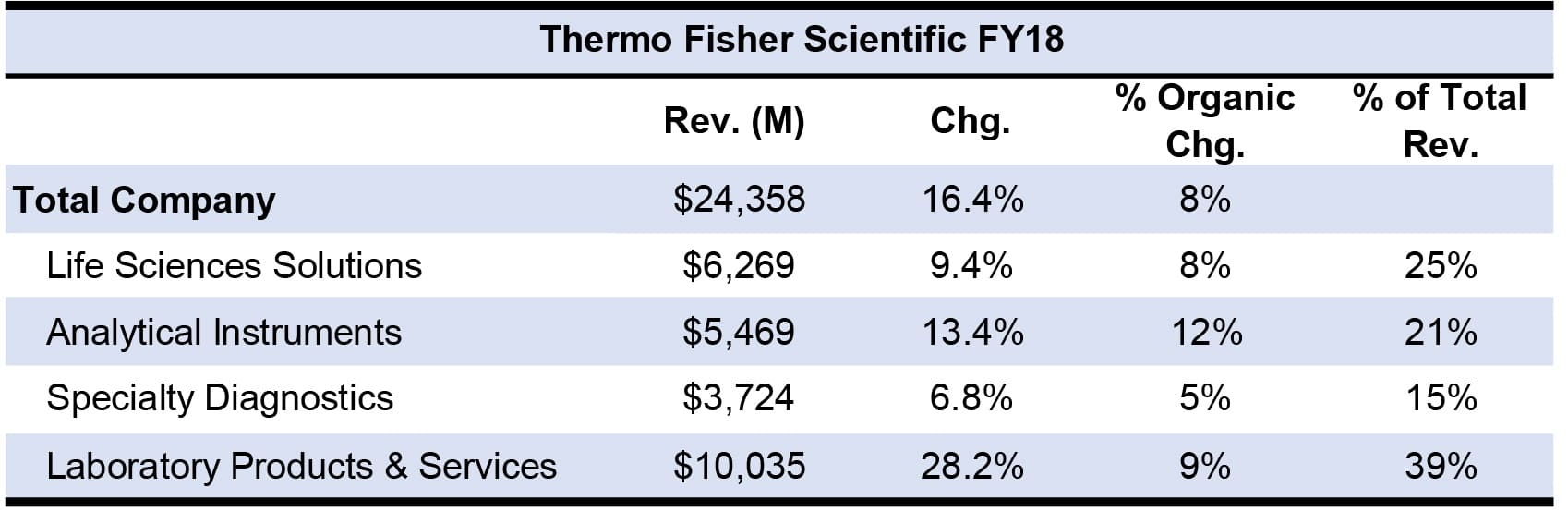

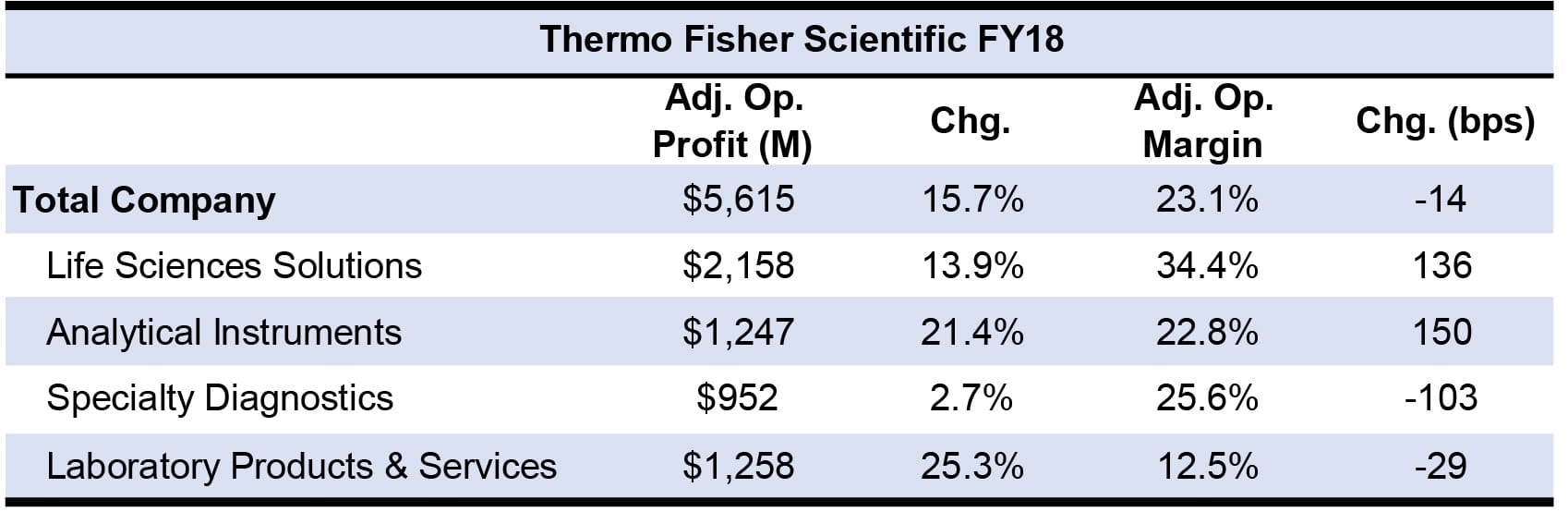

Revenue growth in the Life Sciences Solutions segment was led by bioproduction, bioscience and clinical NGS. The Analytical Instruments segment had broad-based growth across all businesses in the segment. The Specialty Diagnostics segment’s revenue growth was led by the transplant diagnostics, neuro diagnostics and clinical diagnostics businesses, while the Laboratory Products and Services saw broad-based growth across all businesses, especially the pharma services business.

Click to enlarge

Sales to the biotech and pharmaceutical end-market increased in the low teens, while sales to the academic and government end-market delivered mid-single digit growth due to strong sales for the Life Science Solutions and Analytical Instruments businesses. Sales to the diagnostics and healthcare end-markets also grew in mid-single digits led by strong demand in the transplant diagnostics, amino diagnostics and clinical diagnostics businesses. Industrial and applied end-markets’ revenue was up 10%, led by strong demand in the analytical instrument’s businesses.

Click to enlarge

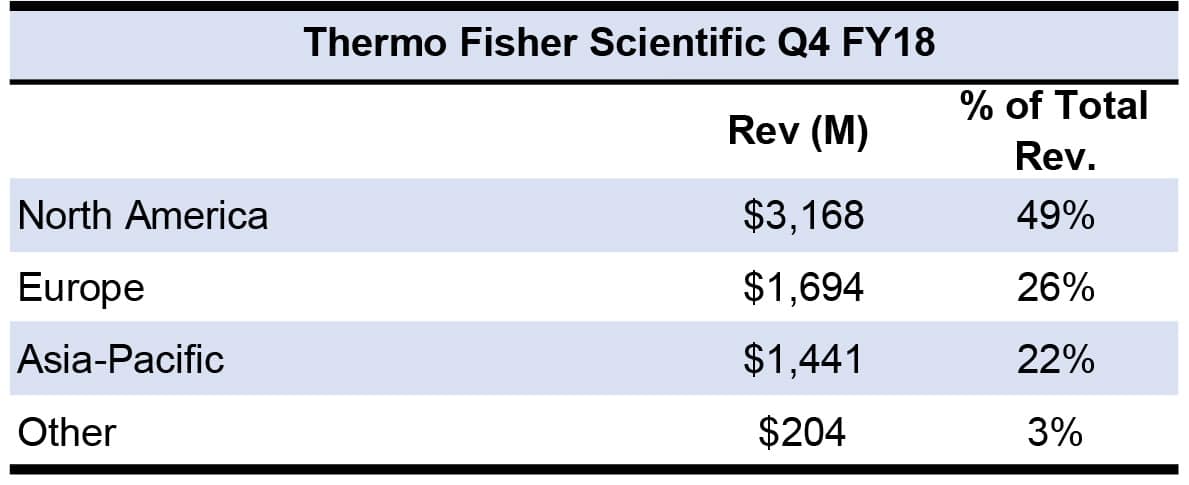

North America and Europe’s revenue growth rose in the high single digits, while Asia-Pacific sales increased in the low teens. Rest of the World sales grew in the mid-single digits. Within Asia-Pacific sales, Chinese sales rose more than 17% to $696 million. Within North America, US sales grew 8% to $3.0 billion.

Click to enlarge

The company did not provide a first quarter revenue guidance.

FYE

Reported double-digit full-year 2018 revenue growth for Thermo Fisher included 7% growth from acquisitions and a 1% decrease from currency. The company also responded to the impact of tariffs by implementing pricing and sourcing actions and adjusting supply chain operations.

Click to enlarge

Sales to the biotech and pharmaceutical end-market increased in the mid-teens, while sales to the industrial and applied end-market delivered high single-digit revenue growth. Both the diagnostics and healthcare, and academic and government end-markets grew in the mid-single digits. Patheon sales increased 10%.

Click to enlarge

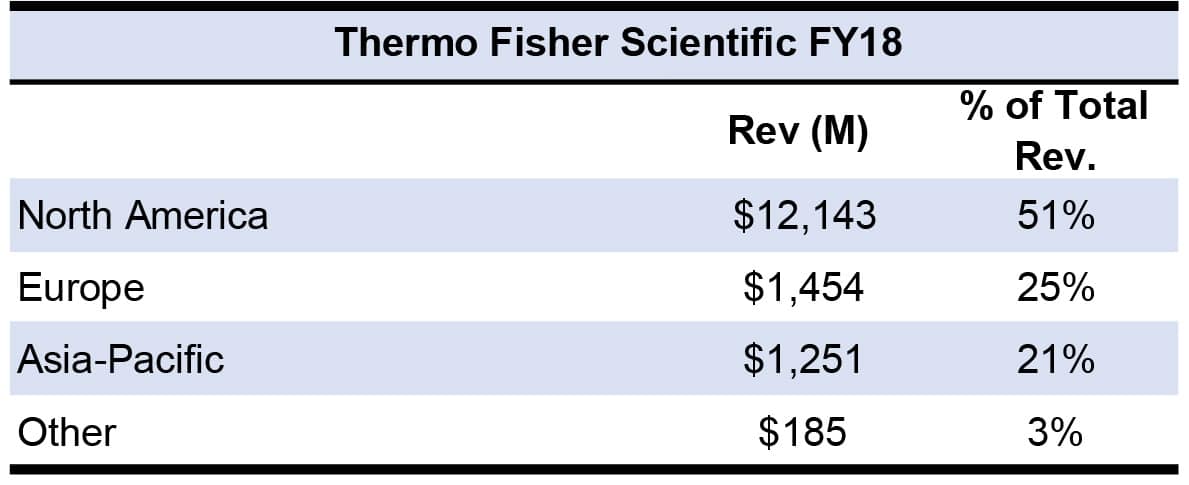

North America sales grew in the mid-single digits, while Europe and the Rest of World revenues increased in the high-single digits. Asia-Pacific sales rose in the mid-teens. Within Asia-Pacific, Chinese sales rose 22% to $2.5 billion while India delivered double-digit sales growth. Sales in high-growth emerging markets accounted for 21% of total revenues totaling approximately $5 billion.

Click to enlarge

The company anticipates its full-year 2019 revenues to grow 2%–4% to $24.88 billion–$25.28 billion, including 5% organic growth and a 1.6% ($400 million) currency headwind. Thermo Fisher took the anticipated slower 2019 GDP performance into consideration for 2019 revenue guidance. Other forecasts include the Advanced Bioprocessing acquisition which the company expects to add $85 million to 2019 total revenues (see IBO 09/15/18). End-marketwise, Thermo Fisher expects high-single-digit revenue growth for the biotech and pharmaceutical end-market, while for academic and government end-market, the company expects low-single to mid-single-digit revenue growth. For the industrial and applied end-market, the company expects a slight decline revenue-wise due to a difficult year-over-year comparison, particularly in the second half of the year. Geographically, Europe is forecast to have low single-digit to mid-single-digit revenue growth.

Click to enlarge