Regional Forecast: Asia and Latin America Strongly Driving Growth

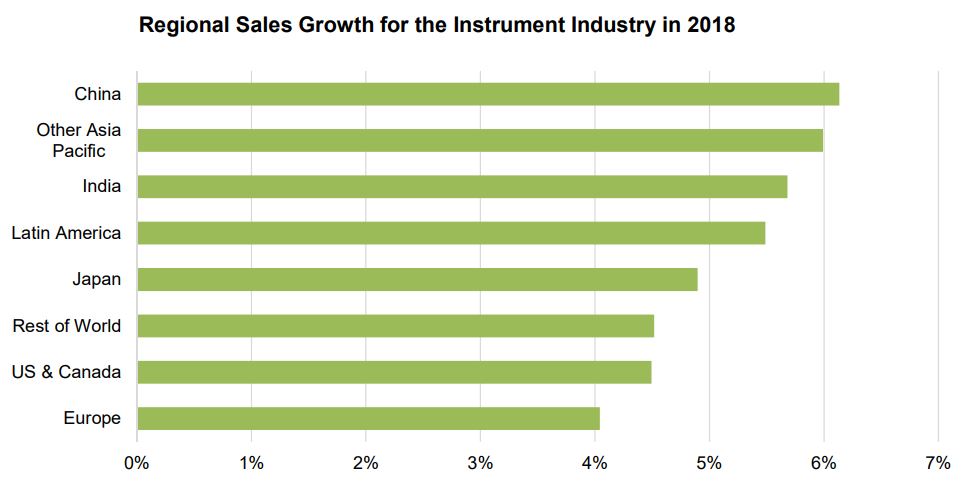

Although both the OECD and the World Bank forecast India to have the highest GDP growth in 2018, this does not necessarily translate into the highest growth for instrumentation. To be sure, India will achieve better-than-average growth for the year, but it will be outshone by China, which continues to present an attractive mix of market size and market growth. Total demand for instrumentation in China is forecast to grow 6.1% in 2018, followed closely by Other Asia Pacific countries and India.

Latin America is poised to spring into a growth mode this year, following some disappointing years hampered by low commodities prices and political instability, both of which had a deleterious effect on Brazil, one of the largest markets in the region. The other primary market, Mexico, was less affected, and is forecast to continue posting stronger growth. Other pockets of innovation exist in Chile and Peru, while other nations are taking a more collaborative approach with joint science and technology programs. Latin America is also looking beyond its shores for help, as evidenced by the joint forum for science and technology between China and the Community of Latin American and Caribbean States (CELAC). They are working to promote technology transfer and collaboration between these regions.

Japan’s research spending combined with an expected currency tailwind should help the country achieve growth above that of the other developed nations. Rising oil prices should help promote increases in spending in the oil-dependent nations of the rest-of-world segment. The US and Canada region is forecast to grow more rapidly than Europe in 2018, but the gap between the two regions will narrow, compared with 2017.

Click to enlarge

Macroeconomic Growth

Global growth in investments and commodity exports helped economic growth activity in 2017, with worldwide economies expected to rebound in 2018, especially in emerging and developing countries. This recovery has resulted in a forecast of global growth in 2018, with major economic organizations such as the World Bank, and the Organization for Economic Cooperation and Development (OECD) indicating average growth of 3.4% (see tables below). However, the positive effects of the economic rebound are predicted to be short term due to potential geopolitical tensions, unstable financial markets, and slowing of growth in emerging markets and developing economies. This short-term positive outlook is reflected in the results of the fourth quarter 2017 Duke/CFO magazine survey, in which the majority of CFOs worldwide cited high optimism levels, but also acknowledged a shift toward focusing on shorter-term projects.

The World Bank forecasts that global economic growth will increase to 3.1% in 2018 due to 2017 surpassing expectations around the world in regards to recoveries made in investment, manufacturing and trade. Although 2018 will continue on this path of improvement, the World Bank cautions that these advancements are short term. The organization defines potential growth as “a measure of how fast an economy can expand when labor and capital are fully employed.” It states that long-term potential growth is likely to be limited due to years of slowing productivity increases, weakened investments and aging workforces worldwide. The impact of this reduction in potential growth is far reaching, affecting 65% of global GDP. It is possible that the deceleration of global growth will last well into the next decade.

For 2018, data indicate that growth in advanced economies (the US, Euro Area, Japan and the UK) is expected to slightly improve to 2.2% due to central banks ceasing their post-crisis policies. Growth in emerging markets and developing economies (East Asia and the Pacific, Europe and Central Asia, Latin America and the Caribbean, Middle East and North Africa, South Asia and Sub-Saharan Africa) will rise to 4.5%, thanks to the recovery of commodity exports.

Similarly, the OECD predicts in November 2017’s “Global Economic Outlook” that annual growth of the world’s economy is set to improve to 3.7% in 2018, but also cites this development as short term. Although the OECD’s data indicate that employment rates have bounced back to those of pre-crisis levels, there have yet to be any concrete gains in wages, as support for monetary policies has decreased. The Organization recommends that private sectors encourage greater productivity, higher wages and more inclusivity to stimulate growth.

Due to the ramifications of Brexit, both tangible and potential, growth in the UK is expected to continue its decline, according to the OECD. But growth in major emerging economies is on an upswing, largely in part as a result of greater infrastructure investments in China; however, growth in these economies is still lower than past recovery levels. Russia and Brazil are respectively recovering and exiting a recession, improving the countries’ economic growth prospects. India’s growth is forecast to surpass China in 2018.

Click to enlarge

Duke/CFO Survey Results

In their December 2017 “Global Business Outlook,” Duke University’s Fuqua School of Business and CFO magazine surveyed approximately 800 CFOS from around the world, including 300 from North America, almost 100 from Asia, 148 from Europe, 215 from Latin America and 55 from Africa. The weighted average projections for capital spending and R&D are divided into global regions below.

Building on last year’s record-breaking Optimism Index, the 2017 survey showed optimism levels of US CFOs to be 69/100 in the quarter, which jumped up to 73/100 after the US Senate passed its tax reform bill, the highest US optimism ever recorded in the survey’s history. The survey’s CFO Optimism Index is considered an accurate estimation of future economic and employment, and therefore GDP growth in the coming year, according to Duke’s Fuqua School of Business.

Innovation was a major global trend in 2017. Nearly 66% of US CFOs claimed more rapid innovation at their firms in the last three years. Because of this quickened pace of innovation and change, 63% of CFOs stated their firms are now focusing more on short-term goals, while 40% stated they are consequently focusing on shorter-lived projects. This is due to attempts to avoid being shackled to long-term investments, especially in the technology sector, where many advancements can quickly fizzle out or become obsolete. By focusing on shorter-term projects, companies have greater flexibility. The rise in innovation increased capital spending at US companies, according to 76% of CFOs, causing 46% to raise R&D budgets and 31% to take on “moonshot” projects.

European optimism spiked in the survey to its highest level in 12 years, jumping to 67/100. Of European countries, the lowest optimism level is in the UK, where it is 58/100. Capital spending in Europe is forecast to grow 4.8% in 2018, with 75% and 67% of respondents increasing capital spending and R&D, respectively.

Asian CFOs hold a solid optimism rate of 66/100, with median capital spending forecast to grow 5% in 2018. Nearly 71% of Asian companies in the survey have increased capital spending due to increased innovation, while 65% and 56% respectively have bolstered R&D spending and moonshot projects.

In China, the optimism level is a high 75/100, with CFOs planning to increase capital spending 2.1% and R&D spending 3.1%. Top concerns for Chinese CFOs include economic uncertainties, government policies and currency risks. These concerns are akin to those of Japanese CFOs, who also cite economic uncertainty and currency risks as possible hurdles. However, optimism in Japan is much lower than in China, with Japanese CFOs giving a cumulative 58/100 score. Despite the lack of optimism, however, capital spending is forecast to increase 8.6% in 2018, with a 4.2% spike for R&D spending as well.

Capital spending in India is also expected to be much higher than China, as the survey results indicated an increase of 10% in 2018. However, Indian CFOs hold the same optimism rating as Chinese executives at 75/100.

Latin American optimism is on the rise, jumping to 73/100, 71/100 and 61/100 in Mexico, Peru and Brazil, respectively. The global innovation trend is present in Latin America as well, according to 63% of CFOs. In response, 67% of Latin American CFOs have increased capital spending, while 52% will boost R&D spending for 2018.