Chromatography: Steady Growth Ahead

Click to enlarge

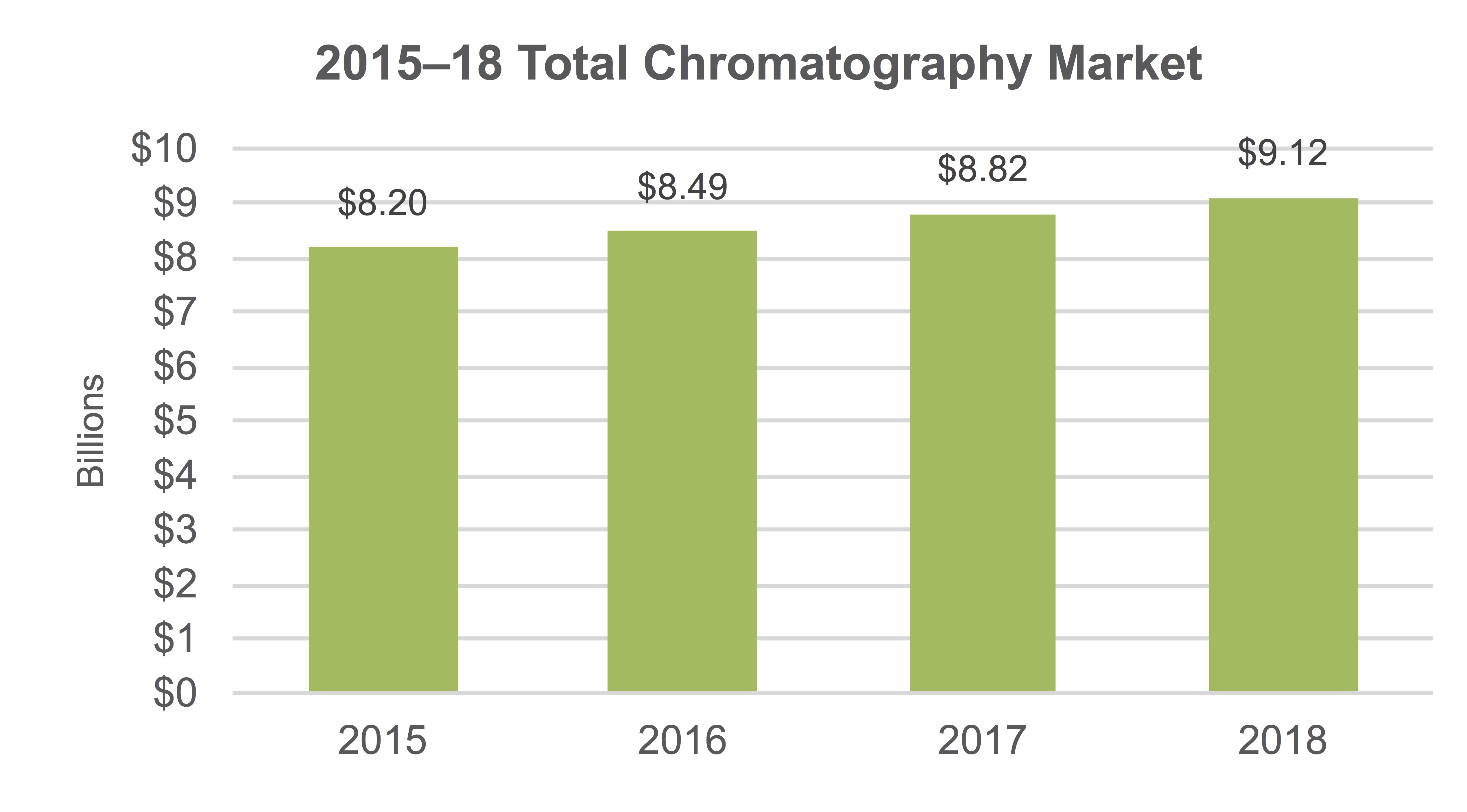

Chromatography sales reached nearly $8.5 billion in 2016, having rebounded from weak growth due to currency effects in the previous year. In 2017, moderate sales increases are expected to continue. With a projected growth rate of 3.9%, the market will be fueled by the rise of clinical chromatography, as well as increased regulations in the pharmaceutical and food industries, particularly in Asia. Almost half of chromatography sales come from the aftermarket, where growth will be strongest.

Click to enlarge

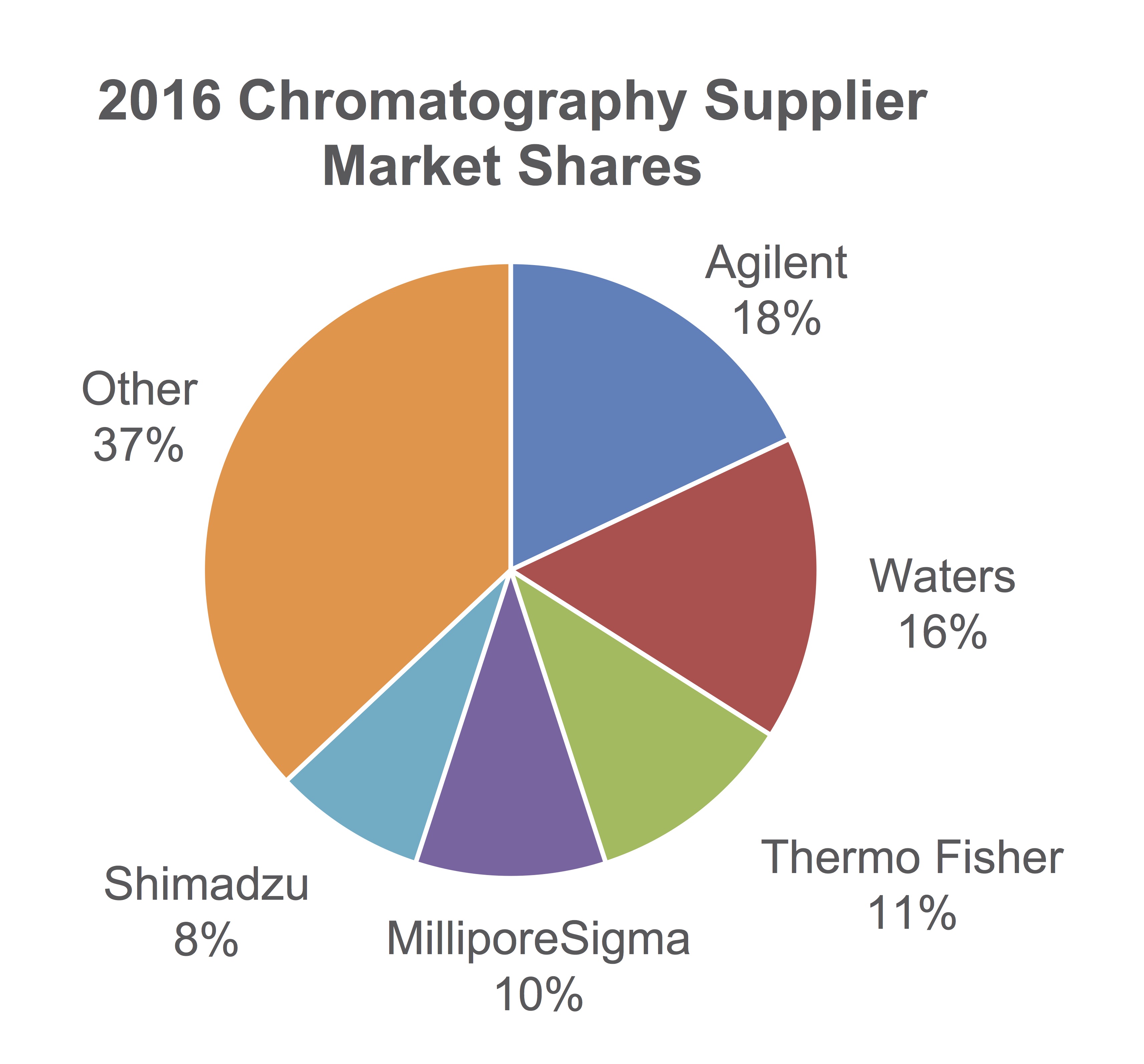

Analytical HPLC is the largest segment of chromatography, covering about half the total market size. Much of the growth here is forecast to come from UHPLC, which in turn is driven by protein-related research applications and QC functions in the pharmaceutical industry. Sales of other types of HPLC systems are expected to grow modestly during the year. Waters remains the dominant vendor in this space, followed by Agilent Technologies. In fact, the companies’ solid occupation of this segment forms the basis of their top positions in the chromatography market as a whole.

Gas chromatography (GC) is the second largest chromatography technology, representing just under a quarter of total sales. Growth for initial systems here will be weak, but aftermarket sales are expected to provide a boost. Environmental testing is likely to contribute strongly to growth, particularly in China. Sales to the pharmaceutical industry and the food industry will also strengthen, but this will likely be offset by weak demand from chemical manufacturers and the oil and gas industry. Agilent is the top vendor for GC, followed by Shimadzu and Thermo Fisher Scientific.

Ion chromatography (IC) sales are heavily dependent on environmental testing and are expected to grow moderately, buoyed by demand from China, India and other Asia Pacific countries. Testing of product impurities in pharmaceuticals, and the agriculture and food industry is also expected to drive growth. Thermo Fisher and Metrohm are the leading suppliers.

Click to enlarge

Sales for preparative HPLC and low-pressure LC (LPLC) are both likely to grow well due to expectations of solid demand from life science applications. Niche applications in the food industry are expected to drive sales for preparative HPLC, while the growth of proteomics research is expected to fuel sales for LPLC. GE Healthcare is the dominant vendor for both of these technologies.

The clinical HPLC market is dominated by Bio-Rad Laboratories and TOSOH. Backed by multiple public health organizations as the gold standard for HbA1c testing and, occupying less than a 5% market share, the technology is poised to experience the fastest growth rate.

Flash chromatography, thin layer chromatography (TLC) and supercritical fluid chromatography (SFC) are the remaining segments. Growth in TLC is expected to be the weakest, cannibalized in part by flash chromatography. The anticipated growth of SFC largely stems from pharmaceuticals, partly due to demand for simplified workflows in testing drug formulations.

Click to enlarge

Click to enlarge