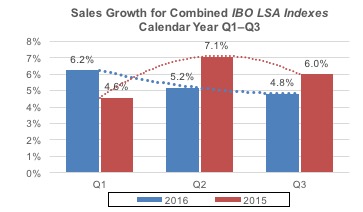

IBO Sales Indexes Resilient in 2016

click to enlarge

IBO’s Life Science and Analytical Instrument Indexes (LSA Indexes) track quarterly sales and operating profit margins for 23 major publicly held instrument and laboratory product companies or businesses. All sales figures are calculated on an organic basis, excluding acquisitions, divestments and currency, and are based on constant exchange rates for foreign companies when converted into US dollars.

In the first nine months of 2016, organic sales growth for companies or businesses in the LSA Indexes remained steadfast, driven by biopharmaceutical, food and genomics applications, as well as notable demand in China. However, challenges in industrial markets, which carried over from the previous couple years, hindered revenue growth for several larger diversified companies. Furthermore, US and European academic and government demand slowed sequentially for a majority of companies in the LSA Indexes during the first three quarters of 2016.

As such, combined organic sales for the LSA Indexes grew 5.4% in the first nine calendar months in 2016, compared to 5.9% in the previous period. Despite a modest deceleration, growth in 2016 was particularly notable given the stronger year-over-year comparison, which included a prominent growth contribution from Illumina in the 2015 period. However, growth for LSA Indexes trended in a sloping trajectory in the first three quarters of 2016, roughly an inverse compared to the previous period, because of the waning academic and government funding.

Biopharmaceutical Markets

Despite the strong year-over-year comparison, biopharmaceutical sales for the LSA Indexes advanced more than 10% organically in the first nine months of 2016. Growth was nearly on par with the 2015 period, driven by technology upgrades and new products for QA/QC, as well as R&D applications. Demand from smaller specialty, CROs and biopharmaceutical customers were particularly robust. Moreover, expanded service and bioproduction revenues for several companies contributed to strength in the biopharmaceutical markets.

Agilent Technologies recorded the strongest biopharmaceutical demand among companies in the Indexes for the second consecutive year, as organic sales expanded 14% in the first nine months of 2016. Thermo Fisher Scientific, Merck KGaA and Waters similarly reported double-digit biopharmaceutical sales growth in the first nine months of 2016. However, growth for this market is expected to ease slightly in the fourth quarter of 2016 as well as in 2017 due to stronger comparisons.

Applied Markets

Applied sales for the LSA Indexes grew roughly in the mid-single digits in the first nine months of 2016 but varied by application. Food sales accelerated throughout the year, driven by expanded regulatory measures in China. For the first nine months of 2016, food sales for both PerkinElmer and Agilent grew double digits. Environmental sales were also positive but grew at a more moderate pace, as several companies reported lower spending towards the latter part of the period. Elevated demand from forensic and clinical markets further contributed to the overall applied market sales growth.

Academic and Government Markets

Academic and government sales for the LSA Indexes were again constrained in the first nine months of 2016, growing in the low single digits due to slowing demand in the US and Europe, as well as sustained weakness in Japan. Waning European academic and government funding surprised several companies in the LSA Indexes, especially in the third quarter, causing certain firms to reassess growth expectations for the region. Waters reported particularly weak third quarter demand for this market, as sales slumped 15% and were down nearly 8% for the nine-month period. In contrast, academic and government spending in Asia, outside of Japan, was healthy. Going forward, European academic and government spending is likely to remain challenged in 2017, while funding uncertainties remain prevalent in both the US and UK.

Industrial Markets

Industrial markets experienced obvious headwinds in the first nine months of 2016, as organic sales for the LSA Indexes contracted roughly 4% due to macroeconomic challenges and delayed equipment purchases. Demand from energy and the metals, minerals and mining industries were particularly vulnerable. Agilent, Bruker, Oxford Instruments and Thermo Fisher each recorded declines in the low to mid-single digits. Industrial sales are expected to return to modest growth in 2017 in view of rising oil and commodity prices, as well as a weak year-over-year comparison.

Geographic Markets

China and India were the most compelling regions in the first nine months of 2016, driven by strong biopharmaceutical, food and environmental demand. Several companies, including Agilent, Thermo Fisher and Waters, reported strong double-digit organic sales growth in each of the two regions. Despite a sequential quarterly decline for most companies in the LSA Indexes, US and European sales each grew in the low single digits in the nine-month period. Japan remained challenged in 2016.

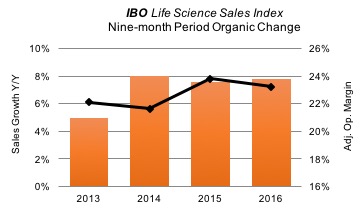

click to enlarge

Life Science Index

The IBO Life Science Index advanced at a robust pace in the first nine months of 2016, as organic sales climbed 7.8%, compared to 7.6% in the previous period. Index growth benefited from strong bioprocess and bioproduction sales for Merck KGaA Life Science and Thermo Fisher. Contributions from clinical and health care–related businesses, as well as higher sales of flow cytometry and cell analysis products, further boosted Index growth. NGS-related sales were mostly healthy, driven by strong recurring revenues, including consumables and services. However, high-throughput instrumentation demand for Illumina tapered due to a strong comparison, order delays and slower academic spending. Adjusted operating margin for the Index slipped 60 basis points to 23.3% in the period, but this was primarily attributed to increased investments.

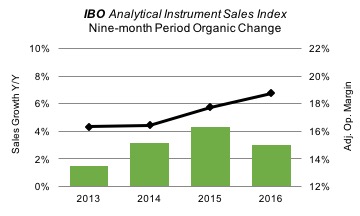

click to enlarge

Analytical Instrument Index

Revenue for IBO’s Analytical Instrument Index advanced 3.0% organically in the first nine months of 2016, compared to 4.3% in the previous period. The strongest growth contribution was in the first quarter, led by demand for LC, MS and lab automation products from biopharmaceutical, environmental and applied markets. However, the slower growth trend was attributed to lower industrial and environment demand, as well as academic and government spending in the second and third calendar year quarters. Adjusted operating margin expanded 100 basis points to 18.7% during the same period due to restructuring activity and cost control measures.