First Quarter 2017 Results: NanoString Technologies, Oxford Instruments, Sartorius, Shimadzu and VWR

Solid First Quarter for NanoString

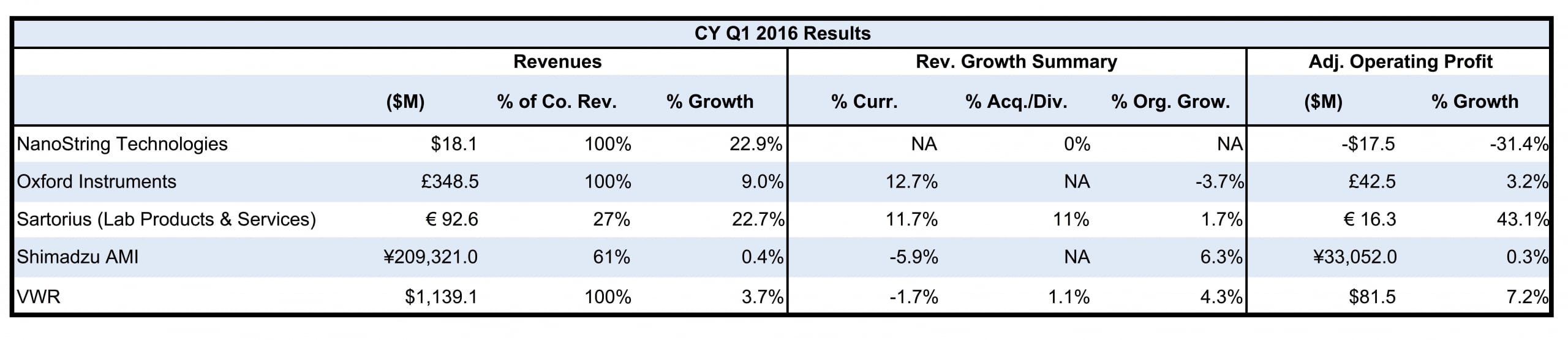

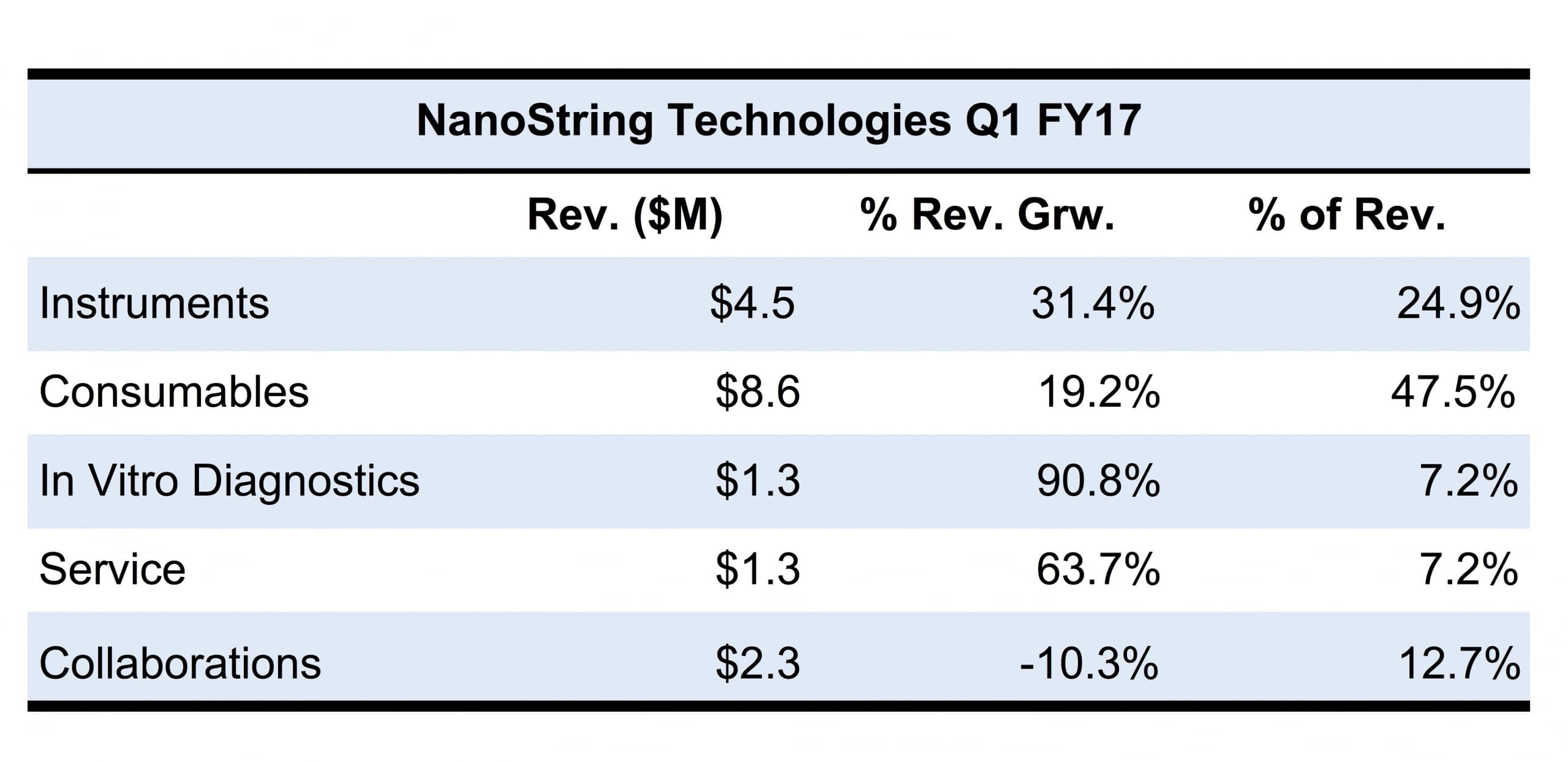

NanoString Technologies posted a strong first quarter, with total revenue of $18.1 million, a 22.9% increase. Collaboration revenue fell 10.3% to $2.3 million and accounted for 12.7% of total revenues. Sales for Product and Service jumped almost 30% to $15.8 million, largely due to the launch of several nCounter products in March (see IBO 3/31/17). Eighty percent of its new systems were sold for precision oncology. The healthy increase in product and service was driven by the strength of biopharma and diagnostics markets, which grew 40% and 90%, respectively, for the company.

Instrument sales grew 31.4% to $4.5 million due to the robust biopharma sector, as NanoString’s installed base increased to an estimated 510 nCounter Analysis systems, surpassing the company’s goal of installing 500 systems for the year. The nCounter SPRINT Profiler systems accounted for approximately half of all instrument units sold, with academia leading demand. Excluding the Prosigna breast cancer assay, consumables revenue jumped 19.2% to $8.6 million, accounting for 47.5% of revenues. Growth was driven by the company’s panel products, which represented over 50% of life science consumables sales, and an increase in the installed base of instruments, with biopharma and CROs accounting for over 40% of consumables revenue.

Click to enlarge

Sales in Asia Pacific slipped 18.4% to $1.4 million, while sales in EMEA jumped 54.7% to $4.4 million, accounting for 7.7% and 24.3% of sales, respectively. Sales in the Americas climbed 21.1%, with US sales representing $11.8 million of total revenue.

NanoString maintained its 2017 revenue guidance of $100–$105 million, which includes a gross margin on product and service between 57% and 58%. The company stated in its conference call that its main objective for this year is the optimization of its commercial capabilities, including new sales staff and advanced marketing tools. For the second quarter, NanoString expects total revenue between $23.5 million and $24.5 million, which includes $18.5–$19.5 million in Product and Service revenue, and approximately $5 million in Collaboration revenue.

Sartorius Lab Products and Services Sales Grow Double Digits

Sartorius first quarter sales grew 13.6%, 12.2% in constant currency, to €343.1 million ($365.0 million). Lab Products & Services (LPS) revenue rose 22.7%, 21.0% in constant currency, to account for 27% of revenues. Acquisitions contributed 11% growth to LPS sales. Orders increased 21.4% in constant currency to €93.4 million ($99.4 million) LPS sales grew in all regions, led by EMEA. Adjusted operating income increased 43.1% to €16.3 million ($17.3 million). LPS constant currency sales growth outlook for 2016 was unchanged at 20%–24%, with organic growth at the midpoint of 5%. EBITDA is expected to increase two percentage points to 16.0%,

Bumpy Year for Oxford Instruments

For the fiscal year ending March 31, Oxford Instruments sales increased 9.0%, down 3.7% in constant currency, to £348.5 million ($452.6 million = £0.77 = $1). Orders grew 12.1% organically but fell 7.3% in constant currency due to the Industrial Analysis and OI Healthcare businesses. Adjusted operating income rose 3.2% to £42.5 million ($55.2 million). Adjusted operating margin declined 70 basis points to 12.2%.

In constant currency, Asian sales jumped 7.2%, but European and North American sales declined 5.9% and 12.0%, respectively.

Nanotechnology Tools (NT) (NanoCharacterization and NanoSolutions) revenues declined organically, but demand in the nanotechnology market was strong, led by next generation batteries and biomedical imaging applications. The academic and metal markets continued to be restrained. Product highlights included robust sales of the XMax Extreme SDD and Imaris analysis software.

Click to enlarge

Asylum Research revenue declined as slower academic funding and product delays affected sales. In the NanoSolutions business, magnet sales and demand related to quantum-related technologies fueled sales. NT adjusted operating profit rose 20.2% to £25.6 million ($33.2 million) as adjusted operating margin expanded 90 basis points to 12.3% due to operational changes and higher-margin products.

Sales for the Industrial Products (IP) segment (X-ray Technology, Magnetic Resonance, Industrial Analysis [divested in April (see IBO 4/30/17)]) also declined on an organic basis. IP adjusted operating margin increased 54.5% to £1.7 million ($2.2 million). Adjusted operating margin rose 100 basis points to 3.0%. Curtailed demand in the oil, commodity and steel markets impacted sales.

Service (general service, OI Healthcare) revenue declined organically as revenue fell for the OI Healthcare business due to a system manufacturer’s revised software licensing policy, which reduced the sale of refurbished systems.

Shimadzu FY17 Sales Boosted by LC and MS

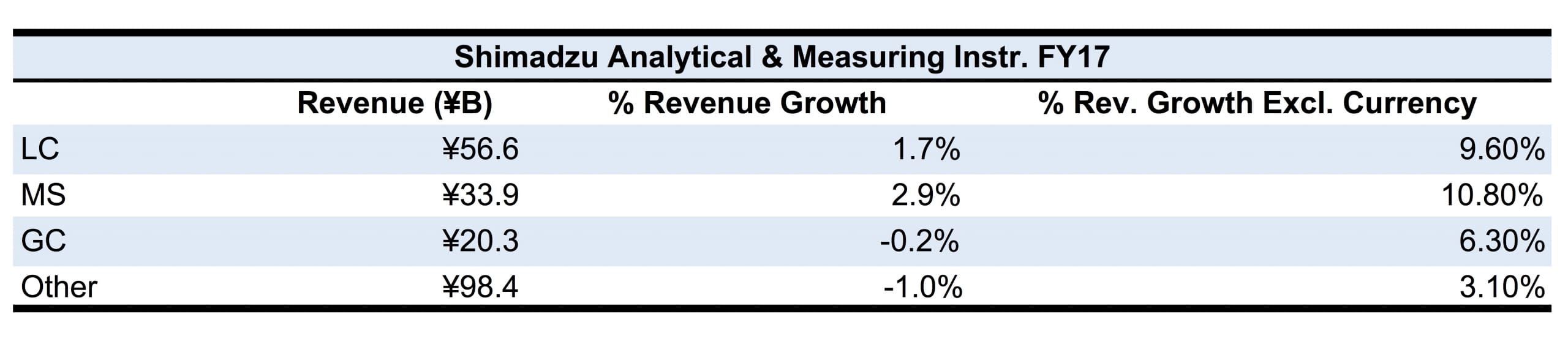

For the year ending March 31, revenue for Shimadzu’s Analytical and Measuring Instrument (AMI) business rose 0.4% to ¥209.3 billion ($1,931.5 million at ¥108.36 = $1), or 61% of company sales. Operating income increased 0.3% to ¥33.1 billion ($305.5 million). Operating margin declined 191 basis points at 15.8%. On a currency neutral basis, AMI sales grew around 6.3%, and operating profit was up 13.4%.

Total FY17 AMI Instrument sales grew 0.1% and were up 6.5% excluding currency. AMI Aftermarket sales grew 1.3% on a reported basis and, excluding currency effects, rose 5.9% to make up 28% of segment sales, up three-tenths of a percentage point.

Click to enlarge

AMI sales in Japan, China and Other Asia Countries rose 5.0%. Excluding currency, Chinese and Other Asian Countries sales rose 1.4% and 2.2%, respectively. AMI Sales in North America and Europe both declined 6.7%, but on a currency-neutral basis, they increased 3.4% and 4.1%, respectively.

Fiscal 2018 AMI sales are forecast to increase 15.9%, up 4.2% excluding currency, to ¥218.0 billion ($2,011.8 million). FY17 priorities for the AMI Business include LC, MS and aftermarket investments, as well as the integration of AMI and Medical Systems product lines as part of a new Healthcare Business Strategy Unit.

Click to enlarge

Under the company’s new Medium-Term Business Plan (FY16–FY19), total AMI revenue is forecast to reach ¥253.0 billion ($2,334.8 million), up 16% from FY16. Within the segment, MS sales are expected to rise 30.6% to ¥45.0 billion ($415.3 million), and LC revenue should increase 26.3% to ¥72.0 billion ($664.5 million). AMI aftermarket sales are expected to make up 30% of total sales, including additional LabSolutions capabilities, and expanded service and consumables businesses. New MS applications will include molecular diagnostics and cell analysis, while new LC applications are expected to be in the area of cell science.

VWR Continues Winning Streak

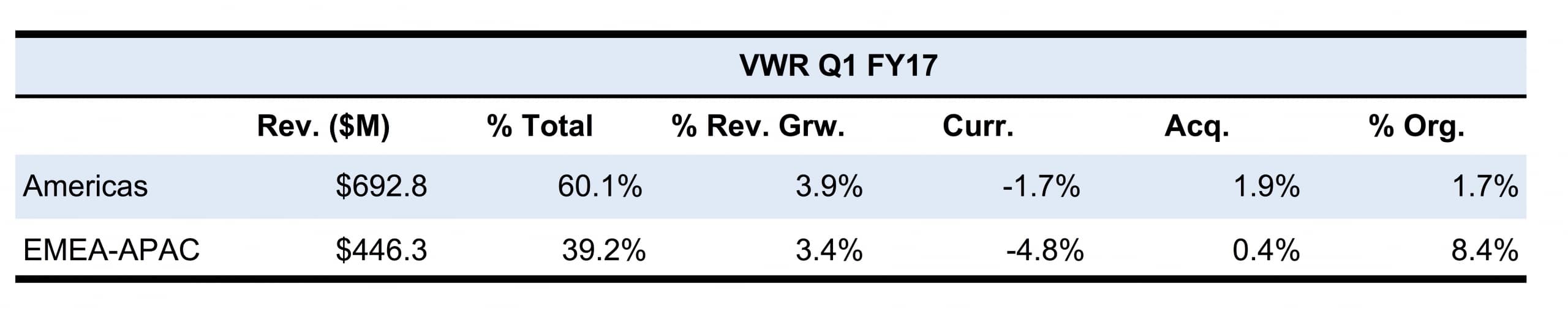

Riding high from the first quarter in 2016, VWR delivered a record first quarter this year, with net sales up 3.7%, 4.3% organically, to $1.14 billion, which were above the company’s long-term expectations of 3-4% yearly organic growth. This is largely due to increasing sales in EMEA-APAC and an improvement of sales in the Americas. Currency reduced net sales growth by 1.7%, or $19.1 million, but was balanced by a 1.1% increase, or $12.5 million, in acquisitions (i.e., Seastar, EPL and MESM) (see IBO 1/15/17, 3/31/17 and 4/15/17).

Due to strong demand from industrial, health care and education customers, VWR’s Americas segment grew 3.9%, 1.7% organically, to $698.2 million, with a 1.9% contribution from acquisitions. Operating margin in the Americas decreased 50 basis points to $41.9 million due to the timing of certain manufacturing orders, as well as $0.9 million in restructuring expenditures and $1.9 million in inventory changes. Sales in education, health care and industrial segments grew in the mid-single digits, while biopharma sales improved in the low single digits. By product, consumables sales grew in the low single digits, while chemicals sales increased in the high single digits. Equipment and instrument sales decreased in the low single digits due to a challenging comparison.

Click to enlarge

VWR’s EMEA-APAC sales grew 3.4%, 8.4% organically, to $446.3 million, but were offset by currency of $20.9 million, a 4.8% decline, while recent acquisitions added $1.7 million, or 0.4% to growth. Operating margin increased 9.0% to $3.3 million and was affected by adjustments in favorable earn-out of $1.7 million and restructuring expenditures of $4.8 million, resulting in an adjusted operating margin of $49.1 million. Biopharmaceutical and government sales grew in the high single digits, while industrial sales increased double digits. Education and health care sales climbed in the mid-single digits. Based on product, sales growth was largely driven by chemicals and other consumables, which increased at double-digit and high single-digit rates, respectively. Sales in EMEA-APAC were furthered by higher volume due to the Easter holiday as well as business trends.

Gross profit margin for VWR decreased 20 basis points to 28.1% largely due to inventory charges, adverse currency effects from cross-border purchasing and product mix. Adjusted operating margin decreased nominally to 7.2%. The company is expected to be fully acquired by Avantor in the third quarter of 2017 (see IBO 5/15/17), and will no longer provide or update financial guidance.