New Report Shows the Impact of the Cell Culture Consumables Market on the Scientific Instruments Industry

Laboratory consumables, non-durable goods used for laboratory-related consumption, enable drug discovery and development and research and production of therapies and vaccines and lately. These products have addressed the COVID-19 pandemic. As a result, consumables offerings are the growth driver of the scientific instrument industry, whose vendors play a crucial role in providing consumables, leading to long-term growth for these companies.

In September 2020, Strategic Directions International (SDi) released the “Global Laboratory Consumables Market.” The report outlines the market conditions in 2019 for consumables used with scientific instruments and in labs. The report provides an overview of the market developments, laboratory applications and regional demand for both the overall market and three product types: life science consumables, cell culture products, and chromatography columns and supplies. This blog focuses on the cell culture sector’s market conditions.

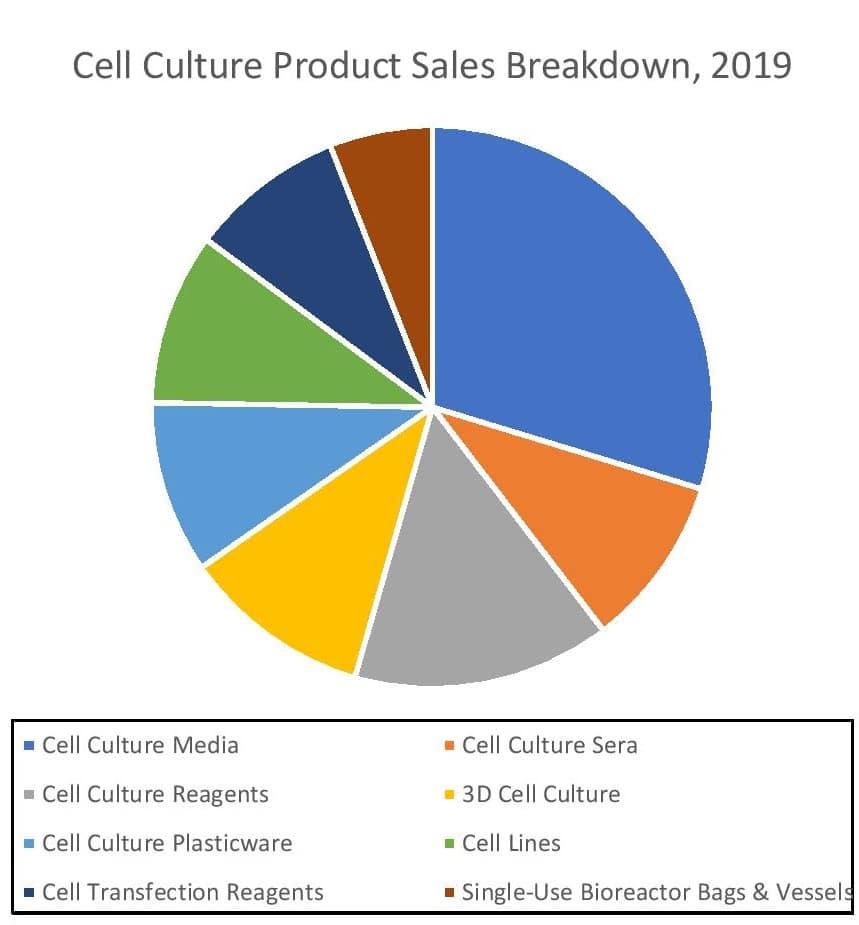

According to the report, the cell culture products market is valued at over $6 billion and is predicted to achieve high single-digit sales growth in the near term. The report divides the cell culture products market into eight product categories: media, sera, reagents, 3D cell culture, plasticware, commercial cell lines, transfection reagents, and single-use bioreactor bags & vessels. The report highlights the leading vendors offering these products, including ATCC, Corning, Lonza MilliporeSigma, and Thermo Fisher Scientific. For the report, SDi utilized primary sources, such as interviews, and secondary resources, including industry publications, online resources and other credible sources.

Among the eight-cell culture product types profiled, cell culture media, 3D cell culture and cell culture reagents were the largest sectors. However, according to the report, cell culture sera, single-use bioreactor bags & vessels, and cell transfection reagents are forecast to be the fastest growing sectors, with demand for single-use bioreactor bags increasing in the double digits, and sales of cell culture sera and cell transfection reagents growing in the high single digits in the short term.

Single-use Bioreactor Bags & Vessels

Single-use bioreactor bags & vessels are the main growth driver for the cell culture consumables market sector because of the products’ key role in bioprocessing. These consumables can shorten the process of cell culture cultivation compared to conventional stainless steel containers. The growing demand for single-use bioreactor bags & vessels stems from the technologies’ advantages in reducing cross-contamination risk, faster implementation and other features. According to the report, pilot (25–200L) products are the critical driver in the expansion of the single-use bioreactor bags & vessel market. China and India are predicted to be the fastest-growing regions in this technology sector. New product introductions are ongoing in this area. In March, Sartorius launched a single-use bioreactor for the biopharmaceutical market to simplify biologics production.

Cell Culture Sera

Regional demand and applied R&D in drug discovery and biotherapeutic development are the primary drivers of the cell culture sera market. The report forecasts demand in the US & Canada and China to increase significantly within this sector. The fetal bovine serum market is projected to fuel growth. Demand for these products is expected to continue because of the product’s low risk of antibody cross-reactions in cell culture cultivation. Thermo Fisher, which sells the Gibco brand, and Cytiva (formerly GE Healthcare), which supplies HyClone offerings, are the top cell culture sera vendors. In November 2019, Thermo Fisher announced it would expand its global bioproduction business, including for its cell culture products, by investing $24 million in its Inchinnan, Scotland, worksite.

Transfection Reagents

Market demand for cell transfection reagents is expected to grow because of their numerous applications in the production of various recombinants, cell therapies, CRISPR/Cas9 systems and more. Additionally, cell transfection reagents play a crucial role in the COVID-19 vaccine race. Along with non-lipid-based transfection reagents, the report predicts lipid-based transfection reagents will be the fastest-growing product segment. For lipid-based transfection reagents, rising interest in applied R&D for drug discovery and clinical trials is the root of strong demand. Once again, China and India are predicted to be the main growth drivers for transfection reagents in general due to both regions’ investment in healthcare infrastructure. In 2019, MilliporeSigma, Roche and Thermo Fisher are the top cell transfection, reagent suppliers. New products are being introduced for the cell transfection reagents sector. This April, Polyplus announced it would launch a transfection reagent product to assist drug development firms in the large-scale manufacturing of cell and gene therapies.

Conclusion

The cell culture products market is projected to significantly contribute to the growth of the overall life science lab consumables market in the near term. In the long term, the report predicts consumables will be an even larger part of drug discovery and other scientific processes.