Scientific Instrument Companies Report First Half Revenue Growth

The scientific instrument industry spans a wide range of techniques, from DNA sequencing to mass spectroscopy (MS) to liquid chromatography (LC), and even the most routine of laboratory products such as balances. The primary function of scientific instruments is basic and applied R&D as well as quality assurance/control. In contrast, diagnostic systems analyze biological samples to determine a medical condition. Applications of scientific instruments range from drug development to food safety testing to the analysis of drinking water. Analytical instruments are also critical to many manufacturing environments, such as quality testing during drug production and petrochemical processing.

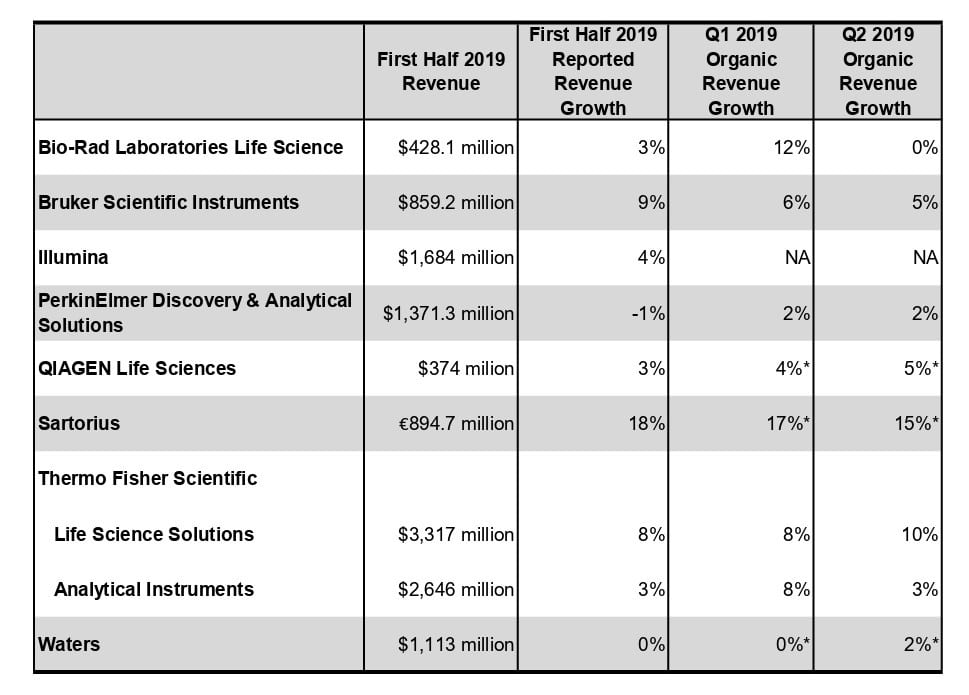

Major publicly held scientific instrument companies recorded solid organic growth in the first half of this year, despite bumps in the road. The table below summarizes revenue changes of these companies (those that have reported quarterly results as of August 1).

*Constant currency

Biopharmaceutical sales continued to be the most robust of any end-market for scientific tool firms. Within this sector, sales in the biotech segment and, regionally, the Chinese research market stood out. In fact, this was very much the story last year as well, indicating the reliability of these markets and their attractiveness to scientific tool vendors. A prime example is Thermo Fisher Scientific Life Science Solutions’ and Sartorius’ bioproduction businesses, for which both companies reported strong results, continuing the growth streak for these segments.

Also on the life science side, companies reported good customer demand for product lines serving the pharmaceutical, government and academic end-markets. These products included Bio-Rad Life Science Solutions’ Droplet Digital PCR systems, Illumina’s high-throughput DNA sequencers, QIAGEN Life Sciences’ automated sample processing systems and Waters’ LC columns.

On the chemical analysis side, Thermo Fisher Analytical Instruments highlighted its LC/MS sales, while PerkinElmer Discovery & Analytical Solutions commented on demand from the fast growing cannabis safety market and Bruker reported healthy growth for its nanoanalysis business.

The weak spots for scientific tool companies in the first six months of 2019 were Europe, and industrial and applied markets. Companies attributed the slower sales growth in industrial markets to market cycles and year-over-year comparisons. In the food market, more than one company cited disruption due to a changeover in China from government to private labs. In Europe, a number of companies described an environment of customer uncertainty due to Brexit, elections and the general macroeconomic outlook.

For other companies, the issues were more specific. Both Illumina and QIAGEN issued pre-earnings press releases announcing slower-than-forecasted second quarter sales growth. Illumina reported an unanticipated slowdown in the direct-to-consumer and populations genomics end-markets. QIAGEN announced the exit of its sequencing partnership for assay development and sales for diagnostic testing in China, which affected its Molecular Diagnostics reporting segment. In spite of these revised expectations, both companies reported revenue growth for the second quarter.

Through the first half of 2019, scientific tool companies remain positive about the fundamentals of their end-markets and product demand. This is expected to drive not only short-term sales growth but long-term sales growth as well.

For access to IBO’s (Instrument Business Outlook’s) updated scientific instrument industry market forecast for 2019, check out the July 31st issue by subscribing now.